How to Maximize Your Credit Card Rewards

I’m going to talk about the problem of what do you do when you’ve maxed out a particular credit card that gives you the most rewards. It’s your favorite card; it’s the one you want. Maybe it’s a mileage card, and you want to keep gaining more miles, but you’ve used to the max of what you can spend for that month. So if it’s a $2,000 a month card, that’s all you can spend, and you can earn miles on the $2,000 you’ve used that month. Now you have to use other credit cards or other means during that month, and then the following month when you pay it off, that was the old way you can now use it again.

Using Your Credit Card Effectively

For example, you got a card and you’ve got a $2,000 limit. What used to happen? Well, what used to happen is, let’s say you would use this during the month, and at the end of that 30 days, you would get in the mail your statement (now you’re probably getting it via email or you’re just logging in), and you would get your statement. And then you would pay that $2,000 off. You’d send in a check or you log into their website, you put in your banking information, and you send over the money. So you’re able to get, let’s say, two miles for every dollar spent. So for that first month, you’re going to get 4,000 miles.

Now let’s talk about the new way you can do it and how you can get many more miles. Here’s what you can do:

- This will represent your 30-day period of time. This is one month here, and you happen to use the maximum which is $2,000, and you use it on the 2nd of the month.

- Okay, there your 2,000 on the second of the month. You just got two times points, so you got 4,000 points. In other words, they gave you two points for every dollar spent, which is fairly common with travel cards, particularly in the airline miles.

So, you got your 4,000 points, and you think this is the 30th day, the end of the month, you think, “Well, that’s all I can get. I maxed out my card. I’m going to pay it off at the end of the month, and I’m going to use it again, and I’ll get 4,000 points every month for a year. Yay! I’m going to get 48,000 points at the end of the year.”

But what if you want to do it faster? Here’s what you can do:

- Go ahead and log in and pay your card off, and then you’ll get to use it again during the month.

- You can literally use it, pay it off, use it again, pay it off, use it again, and pay it off as fast as you can.

Typically what happens is you charge, let’s say on Monday the first. So here’s Monday the first of the month, and you just charge $2,000. You went out and bought your groceries; you got your gas, whatever else you’d like to put on your card. But maybe you spend, let’s say, $6,000 or $8,000 a month on your card, and then you pay it off because you don’t want to have any interest charges. But this card, you can only use $2,000, so you say, “Bummer, I now have to use another card for the other $6,000.” No, you went in; I’m sorry, you used your card, and on Monday the 1st, $2,000. Now typically what’ll happen is when you log into the bank or the credit card company, it’ll show your $2,000 in a pending state, and it’s not quite in the state where you can pay it off, so in a pending state, you may not be able to pay it.

Now you may be able to schedule a payment or send in money, but it still hasn’t cleared. So $2,000 on the 1st, sometimes it might take until the 3rd, and then on the 3rd, it’s no longer in the pending state. Now it shows it as your money owed. So you go ahead, and you’ve already got your banking account information set up; you’re checking your routing number, and you say, “Now pay for my account, pay the $2,000,” so it sends in the $2,000.

As many of you know, it’ll say, “Okay, you’ve authorized us to withdraw $2,000 from your bank account,” but that might take a day or two for it to clear. So it could be until you say, “Go ahead and take my $2,000” on the 3rd; it might be the 5th. I’ve done this on purpose because it’s Monday, Tuesday, 2nd, Wednesday, 3rd, Thursday, and Friday, and I’ll tell you why I did that in a moment. Two days later, it clears, so the $2,000 went in; you now owe 0, and it will say you have $2,000 in available credit. There you go; you didn’t have to wait till the end of the month. You charged it; you sent in the money once it got out of the pending state, and then you paid it off, and it went to zero, and you now have $2,000 available credit. So it’s not the case that you now have to wait till the end of the month to use that $2,000 again.

Now typically, from all the I’ve been doing this for years, I have a business, and I do this with a substantial amount of money, and I do this on the cards that I love. I use them again and again and again and again. But what happens here is usually on Saturday and Sunday, I rarely see movement, so if it takes two days for it to clear, in other words, to get out of the pending state (let’s call that two business days – business days being Monday, Tuesday, Wednesday, Thursday, and Friday), if I’ve charged something on a Friday for $2,000, I don’t see it clear on Saturday, I don’t see it clear on Sunday; it usually takes two more days. So it either be Monday or Tuesday.

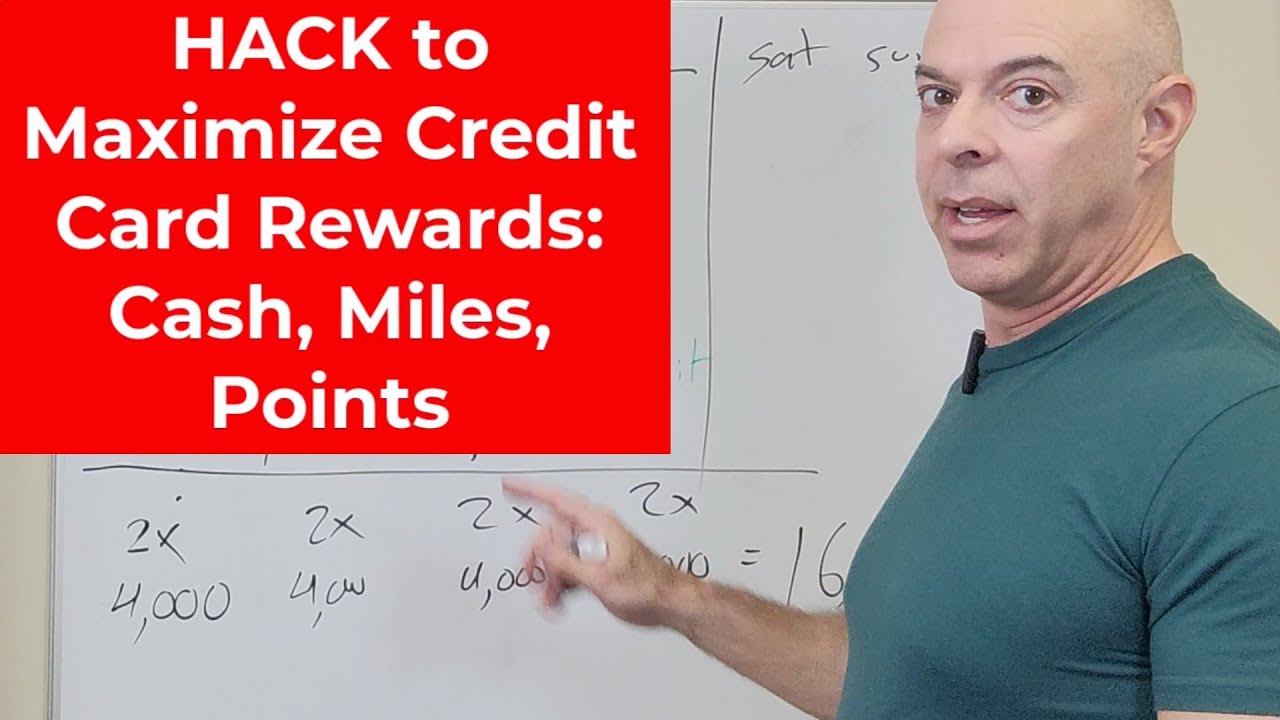

So what does this mean? It means that the best you can usually do is this four times a month because it typically takes five business days, might take four, might take six, depends on when you charge it. But if you were to do this every month on Monday, you could use the card on Monday, then on the next Monday, the next Monday, the next Monday. So potentially, you were able to use it four times.

Instead of just $2,000, and we said you get two points every dollar spent, that’s 4,000 points. Well, now you get to use it the next week, you use it another time, another time, another time. Obviously, that’s another 4,000, that’s another 4,000, my handwriting is amazing, that’s another 4,000. What did you get? You got a total of 16,000. So instead of waiting four months to get 16,000 miles or points, whatever it is you’re getting back from the company, you were able to do it in one month. Now that is what I call maximizing credit card rewards. That’s the solution to being able to utilize the card that you like the most over and over and over again and maximize the rewards from that particular card, and you can do this from what I’ve seen with pretty much every credit card, as long as they allow you to log in and pay online. I hope this helps. Thanks for watching!